by

by In an age of soundbites and sensationalism, the UK property market—particularly here in Crediton—oft...

In an age of soundbites and sensationalism, the UK property market—particularly here in Crediton—often finds itself misconstrued by general narratives.

While we cannot ignore the challenges of increasing mortgage rates and shifting buyer preferences, it is vital to appreciate the broader context to understand what’s happening in the Crediton property landscape.

The UK housing market is currently at a crossroads, characterised by its lowest house price growth since 2012. High mortgage rates are making a significant dent in market activity, affecting everything from buyer demand to the volume of property sales.

Crediton properties are still selling but not at the rate or level they were in 2021. Therefore, correctly pricing your property for sale cannot be underestimated. Let me explain why, then the reasons behind the current state of play nationally, and finally, the exact story of what is happening now (and in the future) in Crediton.

The Importance of Correctly Setting an Asking Price for Your Crediton Home

Putting your Crediton property on the market at too high an asking price can significantly deter potential buyers and limit the number of people who come to view it.

Buyers often have a budget range in mind, and if your property is priced above comparable homes in the area, it’s likely to be filtered out of search results and go unnoticed.

Even if the property gets some attention, the inflated price can send a message that you’re not serious about selling or unwilling to negotiate. This can result in your property languishing on the market, which could necessitate future price reductions.

Over time, a stale listing may become stigmatised, leading buyers to suspect that something must be wrong with the property beyond its high price.

Thus, setting a realistic, market-aligned asking price is crucial for attracting a broad pool of qualified buyers and facilitating a quicker, more lucrative sale.

The Impact of High Mortgage Rates

High mortgage rates are putting a strain on the housing market. The latest data shows a significant fall in demand from buyers — about a third less than the average during the same period over the last five years (2018-2022).

Nationally, this year, the number of properties sold stc has been 750,113 (to the end of August). That same sales figure to the end of August 2022 was 903,799 (a 17% decrease), and to the end of August 2021, 1,020,439 (a 26.49% decrease).

Mortgage-backed sales are particularly hit hard, expected to be just over a quarter lower than last year. Cash sales are expected to be less affected, but the overall market activity remains sluggish.

Regional Disparities

An interesting aspect of the current housing market is the distinct regional disparity. Looking at the £ per square foot of the sales agreed (not completed) of the August 22 sales vs. August 23:

- East of England: -4.85%

- North East: -3.71%

- South East: -2.99%

- Wales: -2.02%

- East Midlands: -1.72%

- Yorkshire and The Humber: -0.85%

- West Midlands: -0.62%

- North West: -0.54%

- Outer London: -0.44%

- Inner London: -0.13%

- South West: 2.85%

- Scotland: 3.88%

In the East of England (as a region), house prices have fallen by just under 5% over the last year. Conversely, there’s been a 3.8% increase in house prices in Scotland.

First-time Buyers and Affordability

High mortgage rates are affecting first-time buyers disproportionately. In 2021/2, low mortgage rates made buying a Crediton home cheaper than renting, spurring a wave of first-time buyers. However, with current mortgage rates soaring above 5%, renting has now become cheaper on average than buying for a first-time buyer property in some regions.

The Role of Wage Growth

Despite the bleak outlook, there is a silver lining. Faster wage growth is making housing more affordable.

Average wage rises of 8.2% over the past year are helping to balance out the effect of higher mortgage payments on first-time buyers’ household incomes. As a result, the gap between house prices and earnings is closing, and affordability is expected to improve by 10% over 2023.

Focus on Crediton

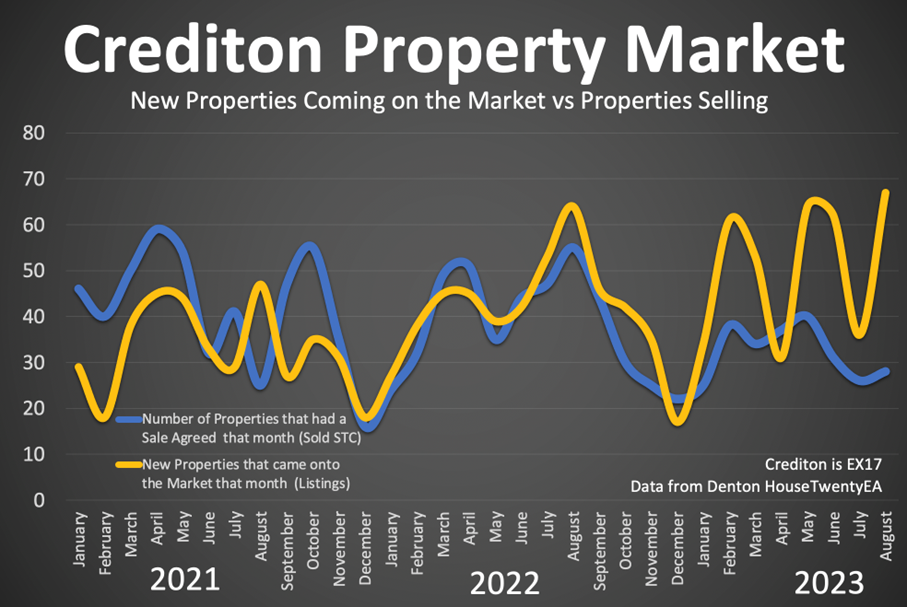

In 2021, an average of 33 properties were coming onto the market in the Crediton area per month, whilst there was an average of 42 properties selling monthly.

In 2022, an average of 41 properties were coming onto the market in the Crediton area per month, yet there was only an average of 38 properties selling each month.

To the end of August 2023, there has been a further increase in new properties coming on the market (an average of 51 properties coming onto the market in the Crediton area per month). Yet, demand has dropped further as only an average of 32 properties have been selling per month.

Note: Crediton = EX17.

The Curse of Overvaluing and How it Could Cost You Your Dream Home

Overvaluing homes is becoming a concerning trend in Crediton, often led by estate agents more interested in listing as many properties as possible rather than making actual sales.

Overvaluing harms homeowners, tempting them with unrealistically high prices only to advise price reductions later. The problem is your dream home might have sold by then.

The Future of the Crediton Housing Market

The immediate future doesn’t hold much promise for dramatic house price growth in Crediton, nor is it expected to fall dramatically.

However, factors like an ageing population, more flexible work arrangements, a strong labour market, and high immigration rates could stir market activity in the next few years.

The UK housing market is navigating through turbulent waters with high mortgage rates and a severe slowdown in house price growth. However, faster wage growth could be a game-changer, making housing more affordable in the long term.

Conclusion

Buyers and sellers can make more informed decisions by understanding these trends and potential future shifts. The market might be under strain now, and homeowners need to be realistic with their pricing; these indicators suggest we might be heading towards a more balanced and accessible market in the coming years.

posted by

posted by

posted by

posted by

posted by

posted by

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link